How to Save Money for Your Big Financial Goals: 5 Simple Steps

Achieving big financial goals often requires disciplined saving and strategic planning. Whether you’re saving for a down payment on a house, a dream vacation, or retirement, having a solid savings plan in place can make all the difference. In this blog, we’ll explore some smart strategies to help you save money effectively for your major financial milestones.

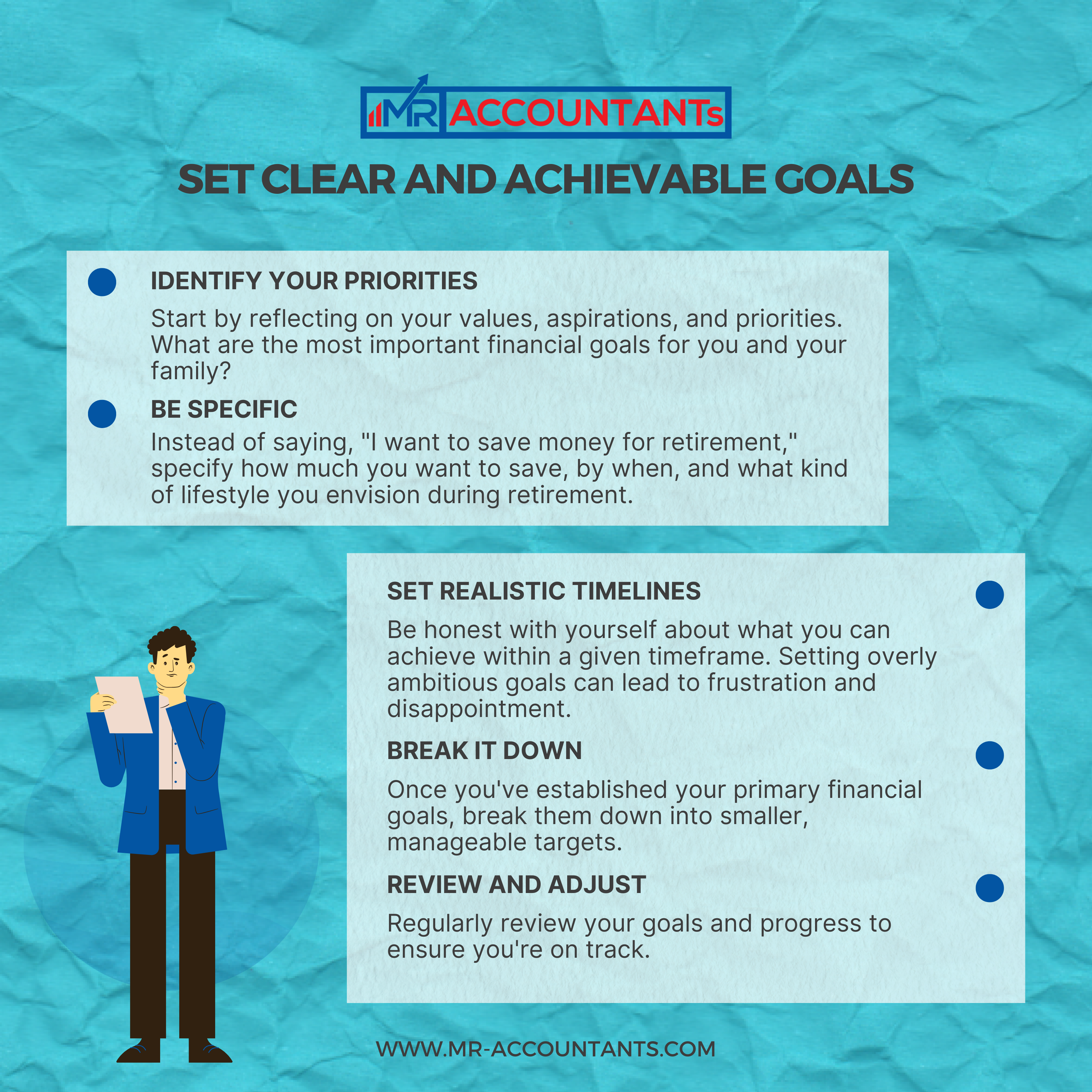

Set Clear and Achievable Goals:

Setting clear and achievable financial goals is the cornerstone of effective saving and wealth-building. Without a clear target in mind, it’s challenging to stay focused and motivated over the long term. Here are some practical steps to help you set clear and achievable financial goals:

Identify Your Priorities: Start by reflecting on your values, aspirations, and priorities. What are the most important financial goals for you and your family? Do you want to own a home, travel the world, start a business, or retire early? Consider both short-term and long-term goals.

Be Specific: Define your goals with as much detail as possible. Instead of saying, “I want to save money for retirement,” specify how much you want to save, by when, and what kind of lifestyle you envision during retirement. The more specific your goals are, the easier it will be to develop a plan to achieve them.

Set Realistic Timelines: Consider the time horizon for each of your goals and set realistic timelines based on your current financial situation, income, expenses, and other obligations. Be honest with yourself about what you can achieve within a given timeframe. Setting overly ambitious goals can lead to frustration and disappointment.

Break It Down: Once you’ve established your primary financial goals, break them down into smaller, manageable targets. Determine what actions you need to take each month or year to progress towards your goals steadily. This could involve saving a certain amount of money each month, paying off debt, or investing in your education or skills.

Review and Adjust: Regularly review your goals and progress to ensure you’re on track. Life circumstances, financial priorities, and external factors may change over time, requiring adjustments to your plan. Stay flexible and adapt your goals as needed while remaining focused on your overarching objectives.

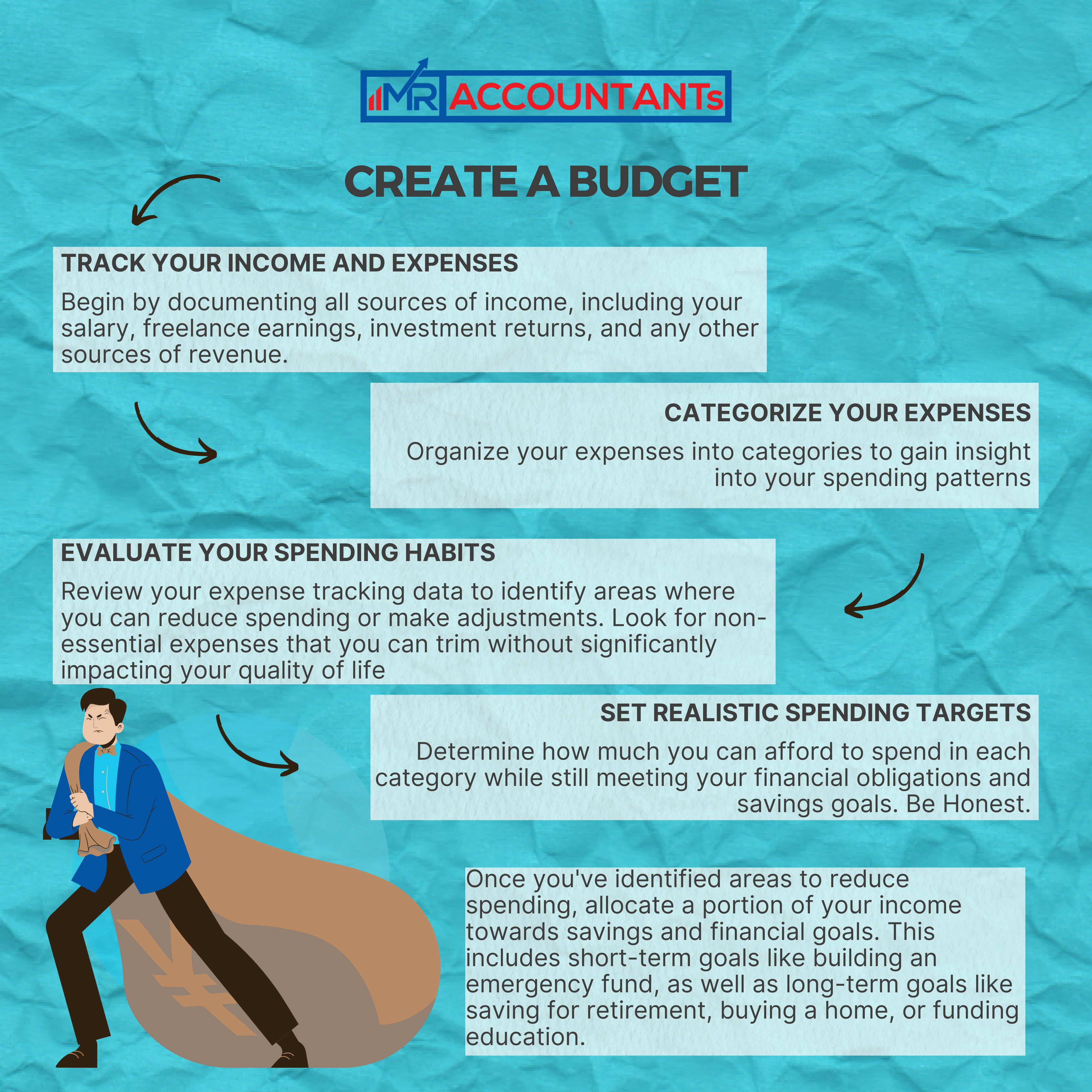

Create a Budget:

Creating a budget is an essential step towards achieving financial stability and reaching your long-term goals. It allows you to understand your financial situation, prioritize your spending, and allocate resources effectively. Here’s a step-by-step guide to creating a budget:

Track Your Income and Expenses: Begin by documenting all sources of income, including your salary, freelance earnings, investment returns, and any other sources of revenue. Next, track your expenses meticulously for at least a month to get a clear picture of where your money is going. This includes fixed expenses like rent/mortgage, utilities, insurance, loan payments, as well as variable expenses like groceries, dining out, entertainment, and transportation.

Categorize Your Expenses: Organize your expenses into categories to gain insight into your spending patterns. Common categories include housing, transportation, food, utilities, healthcare, debt payments, entertainment, savings, and miscellaneous expenses. This categorization will help you identify areas where you can potentially cut back or reallocate funds.

Evaluate Your Spending Habits: Review your expense tracking data to identify areas where you can reduce spending or make adjustments. Look for non-essential expenses that you can trim without significantly impacting your quality of life. This might involve cutting back on dining out, subscription services, impulse purchases, or finding more cost-effective alternatives for certain expenses.

Set Realistic Spending Targets: Based on your income and expense data, establish realistic spending targets for each category. Determine how much you can afford to spend in each category while still meeting your financial obligations and savings goals. Be honest with yourself about your priorities and where you can afford to cut back.

Allocate Funds for Savings and Goals: Once you’ve identified areas to reduce spending, allocate a portion of your income towards savings and financial goals. This includes short-term goals like building an emergency fund, as well as long-term goals like saving for retirement, buying a home, or funding education. Treat savings as a non-negotiable expense and prioritize it in your budget.

Use Budgeting Tools and Apps: Take advantage of budgeting tools and apps to streamline the budgeting process and track your progress. Many apps allow you to link your bank accounts and credit cards to automatically categorize transactions, set spending limits, and receive alerts when you exceed your budget. Choose a tool that aligns with your preferences and financial goals.

Monitor and Adjust Regularly: Budgeting is an ongoing process that requires regular monitoring and adjustments. Review your budget regularly to ensure you’re staying on track and making progress towards your goals. Life circumstances may change, requiring you to adapt your budget accordingly. Stay flexible and be willing to make changes as needed to achieve financial success.

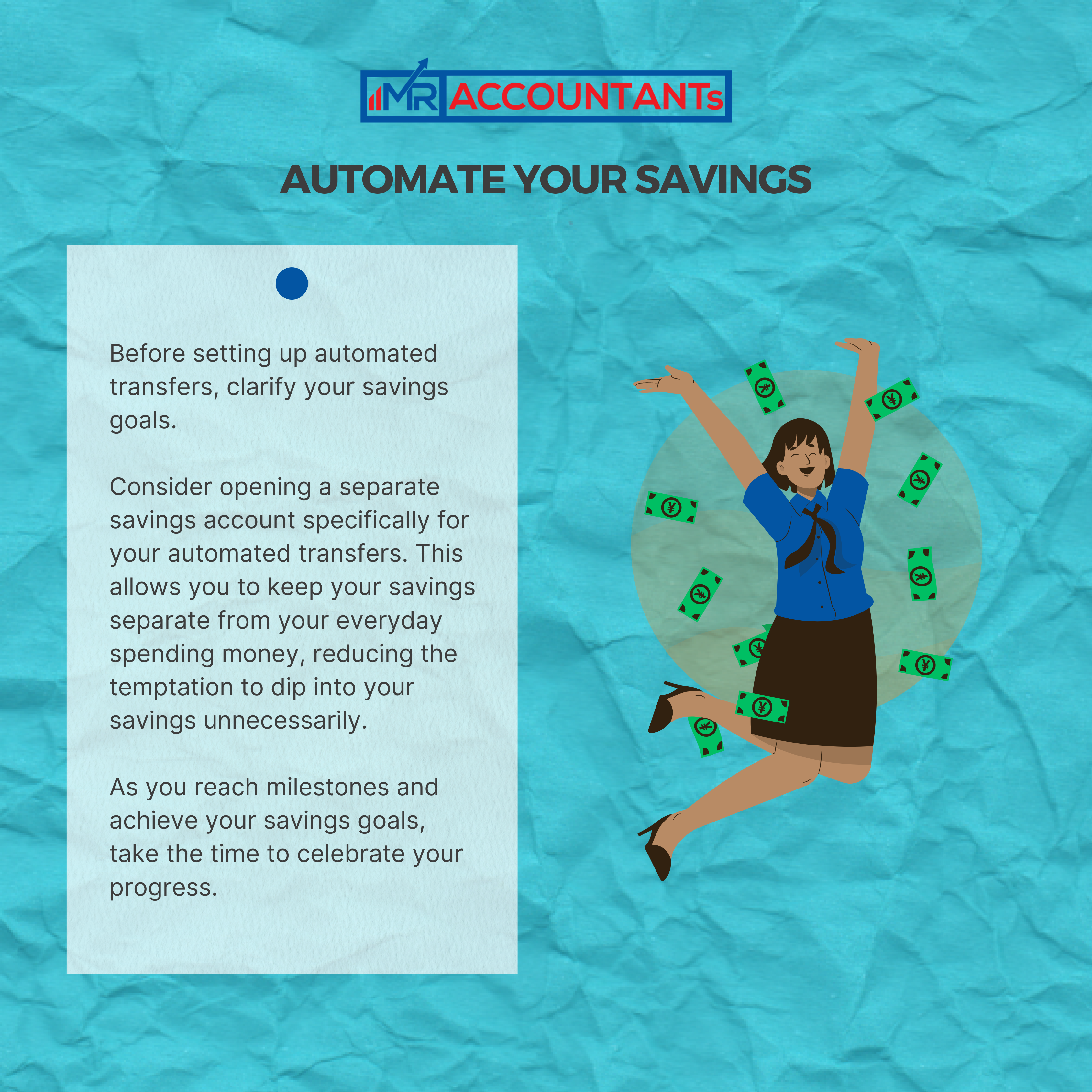

Automate Your Savings:

Automating your savings is a powerful strategy to make saving a consistent and effortless habit. By setting up automatic transfers from your checking account to your savings account, you remove the need for manual intervention, making it easier to stick to your savings goals. Here’s how to automate your savings effectively:

Identify Your Savings Goals: Before setting up automated transfers, clarify your savings goals. Whether you’re saving for emergencies, a down payment on a house, a vacation, or retirement, knowing your objectives will help you determine how much to save and where to allocate your funds.

Choose the Right Accounts: Consider opening a separate savings account specifically for your automated transfers. This allows you to keep your savings separate from your everyday spending money, reducing the temptation to dip into your savings unnecessarily. If you have multiple savings goals, you may want to open multiple accounts, each dedicated to a specific objective.

Set Up Automatic Transfers: Log in to your online banking portal or contact your bank to set up automatic transfers from your checking account to your savings account. You can typically schedule transfers to occur on a recurring basis, such as monthly or bi-weekly, according to your pay schedule. Determine the amount you want to transfer each time based on your budget and savings goals.

Consider Payroll Deductions: If your employer offers direct deposit, you may have the option to split your paycheck between multiple accounts. Consider allocating a portion of your paycheck directly to your savings account to automate your savings even further. This “set it and forget it” approach ensures that a portion of your income goes towards savings before you have a chance to spend it.

Track Your Progress: Monitor your automated savings regularly to ensure that your transfers are occurring as planned and that you’re making progress towards your goals. Review your savings accounts periodically to see how your balances are growing over time. Consider using budgeting apps or spreadsheets to track your savings goals and stay motivated.

Adjust as Needed: Life circumstances and financial priorities may change over time, requiring adjustments to your automated savings plan. If your income or expenses change, or if you have new savings goals, revisit your automated transfers and make any necessary adjustments. Stay flexible and adapt your savings strategy to reflect your current situation and goals.

Celebrate Milestones: As you reach milestones and achieve your savings goals, take the time to celebrate your progress. Recognize your hard work and discipline, and use your achievements as motivation to continue saving for future goals. Whether it’s a small treat or a significant milestone reward, acknowledging your progress can help reinforce positive saving habits.

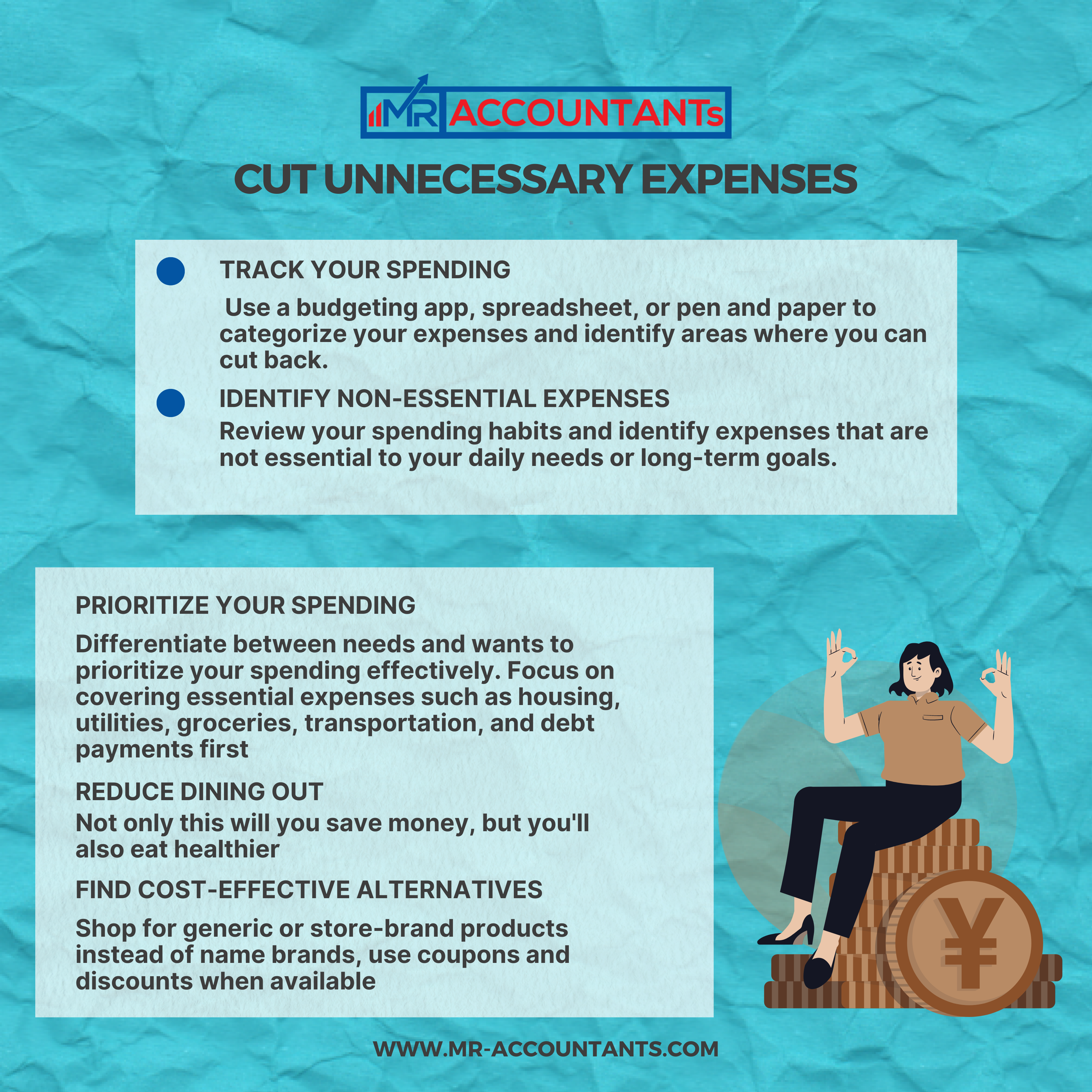

Cut Unnecessary Expenses:

Cutting unnecessary expenses is a practical and effective way to free up more money for savings and achieve your financial goals faster. By identifying and reducing non-essential spending, you can redirect those funds towards your savings priorities. Here’s how to cut unnecessary expenses and save money:

Track Your Spending: Start by tracking your expenses to understand where your money is going each month. Use a budgeting app, spreadsheet, or pen and paper to categorize your expenses and identify areas where you can cut back. This will give you a clear picture of your spending habits and highlight opportunities for savings.

Identify Non-Essential Expenses: Review your spending habits and identify expenses that are not essential to your daily needs or long-term goals. This might include dining out at restaurants, buying coffee or snacks on the go, purchasing clothes or gadgets you don’t need, or subscribing to services you rarely use.

Prioritize Your Spending: Differentiate between needs and wants to prioritize your spending effectively. Focus on covering essential expenses such as housing, utilities, groceries, transportation, and debt payments first. Once your needs are met, allocate remaining funds towards savings and discretionary spending.

Reduce Dining Out: Dining out at restaurants can be a significant expense for many people. Consider cutting back on restaurant meals and instead cook at home more often. Plan your meals, pack lunches for work, and enjoy homemade dinners with your family. Not only will you save money, but you’ll also eat healthier and have more control over your food choices.

Cancel Unused Subscriptions: Review your subscriptions and memberships to identify any that you no longer use or need. This might include streaming services, gym memberships, magazine subscriptions, or software subscriptions. Canceling unused subscriptions can free up extra money each month that you can put towards your savings goals.

Find Cost-Effective Alternatives: Look for ways to reduce the cost of everyday purchases without sacrificing quality. Shop for generic or store-brand products instead of name brands, use coupons and discounts when available, and compare prices before making large purchases. Consider buying items second-hand or borrowing instead of buying new whenever possible.

Set Spending Limits: Establish spending limits for discretionary categories such as entertainment, shopping, and hobbies. Give yourself a monthly allowance for these expenses and stick to it to avoid overspending. Use cash envelopes or budgeting apps to track your discretionary spending and stay within your limits.

Practice Mindful Spending: Before making a purchase, ask yourself whether it aligns with your values and priorities. Consider whether the item or experience will bring you long-term satisfaction or if it’s a temporary impulse purchase. By practicing mindful spending, you can avoid unnecessary purchases and save more money over time.

Monitor Your Progress: Regularly review your spending and savings goals to track your progress and make adjustments as needed. Celebrate your successes and milestones along the way to stay motivated and committed to your financial goals.

Prioritize High-Interest Debt:

Prioritizing high-interest debt is a crucial step towards achieving financial stability and reaching your long-term savings goals. High-interest debt, such as credit card debt, can significantly impact your finances due to the substantial interest charges. Here’s how to prioritize and pay off high-interest debt effectively:

Understand Your Debt: Start by gathering information about all your outstanding debts, including balances, interest rates, and minimum monthly payments. Focus on debts with the highest interest rates, as these are costing you the most money in interest charges over time.

Create a Debt Repayment Plan: Decide on a debt repayment strategy that works best for your situation. Two common methods are the debt snowball and debt avalanche:

Debt Snowball: With the debt snowball method, you prioritize paying off your smallest debts first while making minimum payments on all other debts. Once the smallest debt is paid off, you roll the payment amount into paying off the next smallest debt, and so on. This method provides psychological momentum as you see debts being paid off quickly, which can motivate you to continue.

Debt Avalanche: The debt avalanche method involves prioritizing debts with the highest interest rates first, while making minimum payments on all other debts. Once the highest-interest debt is paid off, you move on to the next highest-interest debt, and so on. This method saves you the most money on interest charges over time, but it may take longer to see progress compared to the debt snowball method.

Increase Your Debt Payments: Allocate as much money as possible towards paying off your high-interest debt each month. Look for opportunities to reduce expenses or increase your income to free up extra funds for debt repayment. Consider cutting discretionary spending, finding ways to save on regular expenses, or taking on a side hustle to generate additional income.

Negotiate Lower Interest Rates: Contact your creditors to inquire about lowering your interest rates, especially if you have a good payment history. Some creditors may be willing to lower your interest rates temporarily or permanently, which can help you pay off your debt faster and save money on interest charges.

Stay Committed and Motivated: Paying off debt requires discipline and perseverance. Stay focused on your goal of becoming debt-free and remind yourself of the benefits of being financially free. Track your progress regularly, celebrate milestones along the way, and visualize the financial freedom you’ll achieve once your debt is paid off.

Avoid Taking on New Debt: While paying off your existing debt, avoid taking on new debt whenever possible. Cut up credit cards or store them away to resist the temptation to use them impulsively. Focus on living within your means and building healthy financial habits that will support your long-term financial goals.

Redirect Freed-Up Funds to Savings: Once you’ve paid off your high-interest debt, redirect the money you were paying towards debt towards your savings goals. Take advantage of the momentum you’ve built to accelerate your savings efforts and work towards achieving your financial aspirations, whether it’s building an emergency fund, saving for a down payment on a home, or investing for retirement.

Achieving big financial goals requires dedication, strategic planning, and disciplined execution. By implementing smart strategies such as setting clear and achievable goals, creating a budget, automating savings, cutting unnecessary expenses, and prioritizing high-interest debt repayment, you can make significant progress towards your financial aspirations. Setting clear goals provides direction and motivation, while creating a budget helps you manage your finances effectively and allocate resources towards your priorities. Automating savings ensures consistency and makes saving effortless, while cutting unnecessary expenses frees up extra funds for savings and debt repayment. Prioritizing high-interest debt allows you to save money on interest charges and accelerate your progress towards financial freedom. Remember that financial success is a journey, not a destination. Stay committed to your goals, regularly review your progress, and make adjustments as needed along the way. Celebrate your achievements and milestones, no matter how small, and keep moving forward towards a future of financial security and abundance. With determination, discipline, and the right strategies in place, you can turn your big financial goals into reality and create the life you’ve always dreamed of. Start taking action today and embark on the path towards a brighter financial future.